Most RV buyers spend more time worrying about the fine print than planning their first trip. In 2024, industry data showed that over 60% of shoppers struggled to distinguish between a direct lender and a finance broker. You want the keys to a Class A or a fifth wheel without the anxiety of a bad deal. It’s natural to feel cautious about good sam rv loans when you’re facing long-term debt on a depreciating asset.

We’re here to provide the clarity you need to move forward. This guide breaks down the Good Sam financing model so you can navigate the application process with total confidence. You’ll discover how to handle requirements for older used models and learn the best way to structure your debt to avoid being upside down. We’ll show you exactly how to compare offers and prepare for a hassle-free exit when you’re ready to trade your title for cash. Let’s get your adventure started with a clear financial roadmap.

Key Takeaways

- Grasp the brokerage model to understand how Good Sam acts as a specialized intermediary between you and the industry’s top lenders.

- Navigate the good sam rv loans process with a clear pre-qualification strategy that identifies your buying power without a hard credit pull.

- Weigh the pros and cons of specialized financing to ensure you secure a competitive rate for your Class A, B, or C motorhome.

- Protect your investment by learning how depreciation curves and full-timer status affect your long-term loan approval and insurance requirements.

- Prepare for a hassle-free exit by discovering how to manage liens and title delays when it’s time to sell your RV for top dollar.

What is a Good Sam RV Loan? Understanding the Brokerage Model

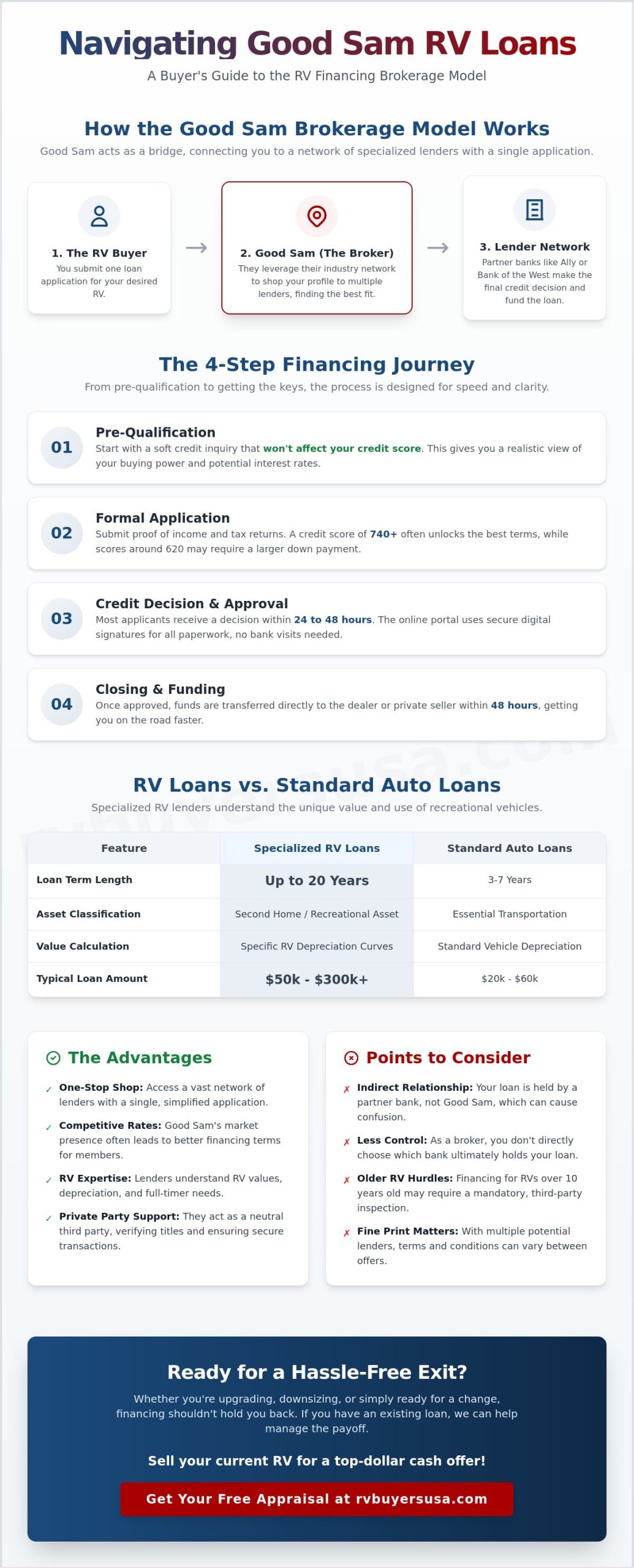

A Good Sam RV loan isn’t a direct product from a single bank vault. Instead, it operates on a brokerage model. Good Sam acts as a high-speed bridge between you and a network of specialized lenders. They don’t lend you the cash themselves. They use their massive industry footprint to find a lender that fits your specific credit profile and vehicle choice. This model simplifies your search. You submit one application, and they handle the heavy lifting of shopping your profile to multiple financial institutions.

Trust is the engine of this process. Since its founding in 1966, Good Sam Enterprises has built a reputation as a cornerstone of the outdoor lifestyle. This brand recognition gives them leverage. Lenders want access to the Good Sam membership base, which often results in more competitive rates for you. Whether you’re looking at a brand-new Class A diesel pusher or a used fifth wheel, good sam rv loans provide a streamlined path to ownership in 2026. They currently offer three primary tracks: new purchase financing, used RV loans for private party or dealer sales, and refinancing options for owners looking to lower their current monthly payments.

The Role of Partner Banks

Your monthly statement won’t usually say Good Sam at the top. Major entities like Ally or Bank of the West actually provide the capital. These partner banks hold your title and manage your payment portal. Good Sam handles the front-end logistics, but the bank makes the final credit decision. This is why you might see a name you don’t recognize on your credit report during the approval process. It’s a standard part of the brokerage setup that keeps the system efficient and nationwide.

Specialized RV Lending vs. Standard Auto Loans

Traditional banks often hesitate when they see a six-figure motorhome request. They view these as high-risk “recreational assets” rather than essential transportation. This classification changes the math for interest rates and down payment requirements. Specialized lenders understand that a Class C motorhome or a travel trailer holds value differently than a sedan. They use specific depreciation curves to calculate your loan-to-value ratio accurately. RV loans typically have longer terms than car loans because the high purchase price of a motorhome requires an extended repayment schedule to keep monthly costs manageable for the average buyer.

Banks specializing in good sam rv loans look at your debt-to-income ratio through a different lens. They recognize that for many, an RV is a second home or a primary residence. This expertise allows for loan terms that can stretch up to 20 years for qualified buyers. You won’t find that kind of flexibility at a local credit union that only handles commuter cars.

How the Good Sam Financing Process Works in 2026

Securing good sam rv loans starts with clarity. You need to know your budget before you fall in love with a coach. The process begins with pre-qualification. This step uses a soft credit inquiry. It won’t hurt your credit score. It gives you a realistic look at your buying power. Once you choose a Class A or Class C motorhome, the formal application begins. You will provide tax returns and proof of income for high-value loans. This is standard for luxury assets. Lenders look for stability. If your credit score sits between 600 and 750, expect tiered interest rates. A 740 score often unlocks the most competitive terms available in 2026. A 620 score might require a larger down payment or a shorter loan term. Always review consumer advice from the FTC to understand how APR impacts your total cost. Closing happens quickly. Money moves directly to the dealer or the private seller within 48 hours of final approval.

The Online Application Journey

The Good Sam Finance Center portal is built for speed. Start by entering your personal details and the RV’s specific specs. Most applicants receive a credit decision within 24 to 48 hours. The system uses secure digital signatures for all paperwork. You can sign your loan documents from your smartphone. This eliminates the need for overnight mail or physical bank visits. It’s a streamlined path to ownership. If the financing process feels overwhelming, you can always sell your current RV for cash to simplify your next down payment and reduce the amount you need to borrow.

Financing Private Party Transactions

Good Sam handles the heavy lifting for private sales. They act as a neutral third party between you and the seller. This service is vital for title verification. They ensure the title is clear of liens before any money changes hands. An inspection is usually required for units over 10 years old. This protects your investment from hidden mechanical issues. They use safe money transfer protocols to protect both parties. The seller gets paid securely. You get the keys without the risk of a fraudulent transaction. It’s a professional way to buy outside of a dealership environment. Good sam rv loans make the private market accessible and safe for every buyer.

The Pros and Cons of Choosing Good Sam for Your RV Loan

Good Sam operates as a specialized broker rather than a direct lender. This distinction is vital for your financial strategy. They connect you with a network of banks that specifically handle recreational vehicle debt. This specialized focus helps when you are looking for good sam rv loans to cover high-value assets like Class A motorhomes or luxury fifth wheels. Traditional banks often view these as high-risk lifestyle purchases, but Good Sam treats them as standard collateral. Understanding how to finance an RV requires looking at both the convenience of these networks and the potential costs involved.

Why Specialized Financing Wins

Specialized lenders understand the longevity of a well-maintained diesel pusher. While a local bank might limit you to a five-year term, Good Sam offers access to 20-year loan terms. This keeps your monthly payments manageable on six-figure purchases. They also handle the heavy lifting regarding nationwide registration and titling. You won’t have to navigate the complex paperwork alone. Their team knows the difference between a travel trailer and a park model, ensuring your loan matches the specific asset type perfectly.

- Older RV Support: They often finance units up to 10 or 12 years old.

- Longer Terms: 15 to 20-year options are common for loans over $50,000.

- Ecosystem Perks: Easy integration with specialized insurance and 24/7 roadside assistance.

Potential Red Flags to Watch For

Don’t let the low “starting at” APR fool you. These rates are typically reserved for borrowers with credit scores above 740 and significant down payments. You must account for potential broker fees or origination costs that aren’t always front-and-center. The biggest risk with good sam rv loans is the long-term debt structure. A 20-year term means you pay significantly more in interest over time. It also increases the chance of being “upside down,” where your loan balance exceeds the RV’s depreciated market value.

Get a clear breakdown of all processing fees before you commit. Some lenders in their network may charge prepayment penalties if you try to exit the loan early. Always compare the total cost of the loan, not just the monthly payment. This transparency ensures you stay in control of your adventure without financial surprises down the road. Stick to the facts, check the fine print, and move forward with confidence.

Critical Factors to Consider Before Signing Your Loan

Buying an RV is a major investment. You need to understand the financial mechanics before you commit to a long-term contract. RVs are depreciating assets. A new motorhome loses approximately 20% of its value the moment it leaves the dealership lot. By the end of year three, that depreciation often hits 30% to 35%. This creates a massive risk of becoming “upside down” on your loan, where you owe more than the rig is worth. This is why good sam rv loans often require a solid down payment. Aim for 10% to 20% down. This 2026 gold standard ensures you maintain equity even if the market shifts unexpectedly.

Tax benefits remain a significant advantage for savvy buyers. Most RVs qualify as a second home if they have permanent sleeping, cooking, and toilet facilities. Under current IRS rules, you can deduct the interest on good sam rv loans just like a traditional mortgage. This deduction applies to total debt up to $750,000. It turns your adventure vehicle into a legitimate tax shield, reducing your effective annual cost of ownership. Always verify your specific eligibility with a tax professional before filing.

Total Cost of Ownership Beyond the Payment

Your monthly payment is only the starting point. Owners must account for insurance, specialized storage, and routine maintenance. Follow the “Rule of Thumb” for RV budgeting: set aside 2% of the vehicle’s purchase price for annual repairs. For a $100,000 Class A motorhome, expect to spend $2,000 a year on upkeep. Avoid the trap of ultra-long loan terms. A low monthly payment over 20 years can result in paying for the RV twice once interest is factored in. Keep your term as short as your cash flow permits to build equity faster.

Full-Timer Financing Nuances

Lenders view full-time living differently than weekend camping. If you don’t have a permanent bricks-and-mortar address, some banks will deny your application immediately. They see the lack of a fixed residence as a high credit risk. You must establish a legal domicile in states like South Dakota, Texas, or Florida to satisfy residency requirements. These states offer mail forwarding services that lenders recognize as valid addresses.

Financing for full-timers also requires specific insurance. A standard recreational policy won’t satisfy lender requirements for a primary residence. You need a full-timer package that includes personal liability coverage similar to a homeowners policy. Understanding the full scope of good sam insurance coverage is essential before you sign your loan documents, as lenders will verify this coverage before they fund the deal. If you want to skip the financing headache and get cash for your current rig instead, you can sell your RV fast with our streamlined process.

The Exit Strategy: Selling an RV with a Good Sam Loan

Selling an RV with an active loan adds layers of complexity to your exit strategy. When you finance through good sam rv loans, the lender holds a legal lien on the title. You don’t own the vehicle outright; the bank does. This means you cannot simply sign over the title to a private buyer in a driveway. Most private buyers in 2026 are wary of title-in-transit scenarios. They want the physical title immediately upon payment. If you still owe money, the bank won’t release that document until they receive the full payoff amount. This creates a deadlock. The buyer won’t pay without a title, and you can’t get the title without their payment.

Negative equity is another hurdle for many owners. According to J.D. Power data from 2024, some RV models lose 20% of their value in the first year alone. If your loan balance is higher than the current market value, you must pay the difference out of pocket to clear the lien. Private sales often fall apart at this stage because buyers don’t want to wait 15 to 30 days for a bank to process the paperwork and mail the title.

Clearing the Lien for a Clean Sale

You must request an official payoff quote from your lender to start the process. This document is typically valid for 10 days. If you find a private buyer, you’ll need to coordinate a meeting at a local bank branch or use a third-party escrow service. These services often charge fees ranging from $200 to $500. Private buyers are often hesitant to deal with bank-owned titles because of the risk and the administrative burden. One mistake in the paperwork can lead to months of delays at the DMV.

The RV Buyers USA Advantage

Don’t let a bank lien stall your plans. We specialize in buying Class A, B, and C motorhomes, fifth wheels, and travel trailers with existing good sam rv loans. Our professional team removes the friction from the sale. We handle every piece of bank and DMV paperwork for you. You don’t need to spend weeks coordinating with lenders or worrying about title delays. We provide a professional exit strategy that protects your credit and puts money in your pocket.

- We handle the entire loan payoff process directly with your lender.

- Our team manages all DMV title transfer paperwork.

- We offer nationwide service and come directly to your location.

- Get paid quickly without the stress of private showings.

Get an instant cash offer today. We come to you anywhere in the country. Our process is fast. We pay top dollar and settle the loan directly with your lender. You get a clean break without the stress of private listings or dealership low-balls. We handle the heavy lifting so you can move on to your next adventure. Our goal is to make your exit as smooth as your first trip.

Take Control of Your RV Journey Today

Success with good sam rv loans in 2026 requires a firm grasp on the brokerage model and how it impacts your long-term equity. You now understand the trade-offs between their convenient application process and the complexities of managing a third-party bank lien. As the 2026 market continues to shift, staying informed about your specific loan structure ensures you aren’t trapped when it’s time to upgrade or sell. Whether you own a fifth wheel or a luxury motorhome, having a professional exit strategy is just as vital as the initial purchase.

Don’t let the stress of bank payoffs or DMV red tape stall your progress. We specialize in stripping away the anxiety of selling a financed asset. Our experts provide professional appraisals based on real-time market data to ensure you get a fair deal without the typical dealership runaround. We handle the entire bank lien payoff and all required paperwork. Our team offers nationwide pickup and travels to your location anywhere in the US. Get a Top-Dollar Cash Offer for Your Financed RV Today and experience a truly no-hassle transition. Your next great adventure is waiting for you.

Frequently Asked Questions

What is the minimum credit score for a Good Sam RV loan?

You can qualify for financing with a credit score as low as 600 through Good Sam’s network of lenders. However, the most competitive interest rates in 2026 are reserved for borrowers with scores of 740 or higher. This tiered system ensures that many travelers get on the road while rewarding those with excellent credit history with lower monthly payments and better terms.

Does Good Sam finance older RVs?

Good Sam often provides financing for RV models that are up to 12 years old. You’ll find that older units typically come with shorter loan terms and slightly higher interest rates compared to brand-new inventory. For instance, a 10-year-old Class A motorhome might only qualify for a 120-month term, whereas a new model could reach a 240-month term for lower payments.

Can I use a Good Sam loan for a private party sale?

You can definitely use good sam rv loans to purchase a vehicle from a private individual. Good Sam is one of the few major brokers with a dedicated process for person-to-person transactions. They handle the title work and lien payoffs directly, which removes the stress and security risks usually found when buying from a seller on a marketplace or classified site.

Are there prepayment penalties on Good Sam RV loans?

Most partner lenders in the Good Sam network don’t charge prepayment penalties, so you can pay off your balance early without extra fees. You should still verify this specific detail in your final contract before signing. Paying an extra $100 toward your principal each month can significantly reduce your interest costs and help you build equity in your motorhome much faster.

What is the typical down payment required for an RV loan?

A standard down payment for an RV loan ranges from 10% to 20% of the total purchase price. While zero-down programs exist for borrowers with credit scores above 800, putting 20% down is the smartest way to avoid immediate negative equity. This initial investment ensures your loan balance stays closer to the actual market value as the vehicle depreciates over the first 24 months.

How long are the loan terms for a motorhome?

Loan terms for motorhomes typically range from 5 to 20 years depending on the loan amount and vehicle age. Loans exceeding $50,000 often qualify for the 240-month term to keep your monthly budget manageable. Smaller loans for travel trailers or older units usually fall into the 5-year to 12-year range. Shorter terms help you build equity faster and pay less total interest.

Can I refinance my existing RV loan through Good Sam?

You can refinance your current RV loan through Good Sam to lower your monthly payments or capture a better interest rate. This is a great move if your credit score has improved by 50 points or more since your original purchase. The refinancing process is fast and can often be completed online, helping you keep more cash in your pocket for your next road trip.

What happens if I owe more on my RV than it is worth?

If you’re “upside down” on your loan, you must pay the lender the difference to clear the title before you sell. This situation is common with 10% down payments and rapid depreciation. To skip the hassle of a private sale, work with RV Buyers USA. We come to you nationwide with an instant cash offer and handle the complex payoff paperwork for you.