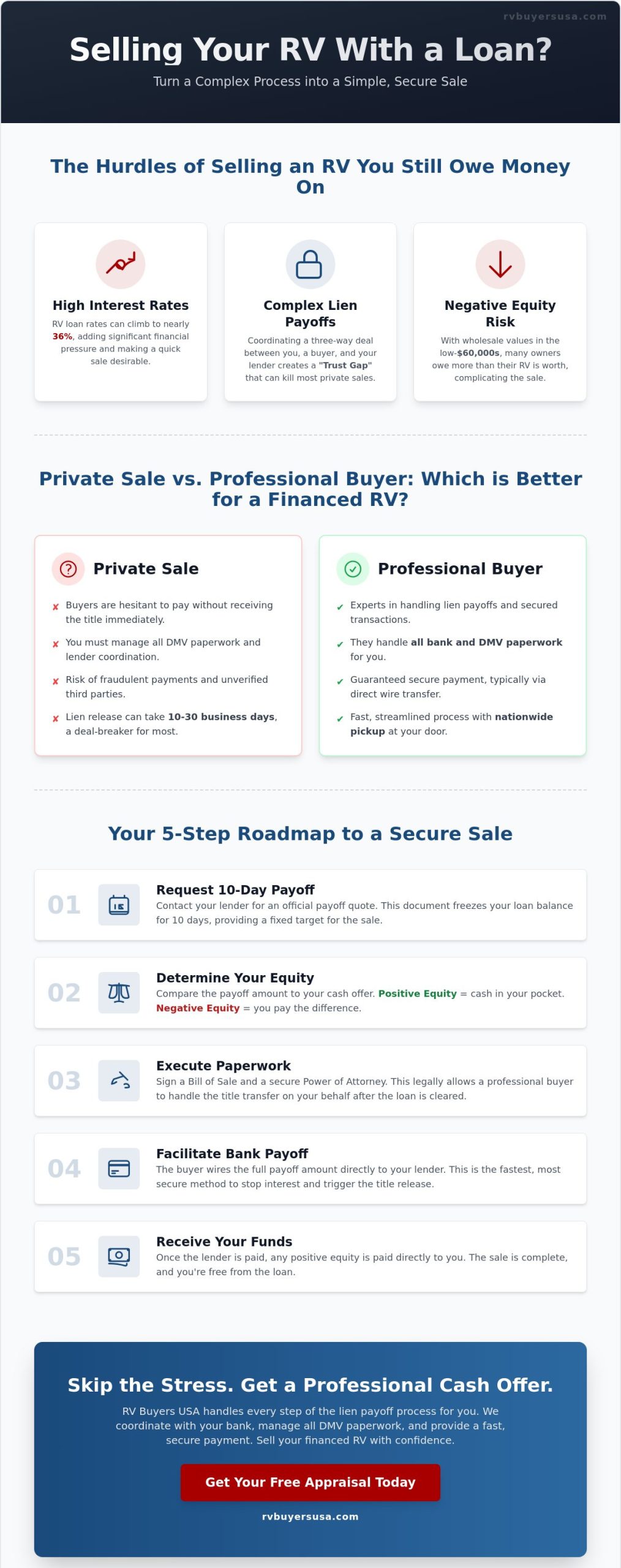

Most owners believe their bank holds the keys to their freedom as long as they have an outstanding loan. It’s a common myth that selling a motorhome I still owe money on is a legal nightmare or a financial trap. You’re likely feeling the weight of high interest rates, which can hit nearly 36% for some RV loans in 2026. It’s stressful to manage bank lien logistics or worry about being underwater when motorhome wholesale values are hovering in the low-$60,000 range.

We understand that anxiety, but a bank lien is just a paperwork hurdle, not a barrier to a fast cash sale. You can clear that debt and walk away with a fair price without the typical dealership headaches or private buyer flakes. This guide shows you exactly how to handle the DMV paperwork and exit your loan securely, even if you owe more than the current market value. We’ll break down the 2026 steps to coordinate with your lender, manage state-specific title fees, and secure a professional cash offer that brings the buyer right to your door.

Key Takeaways

- Master the logistics of selling a motorhome I still owe money on by understanding how your lender manages the title release process.

- Get the exact steps to request a 10-day payoff and determine if you have positive or negative equity in your vehicle.

- Learn why professional acquisition is faster and more secure than trying to coordinate a bank payoff with a private buyer.

- Identify your options for clearing a lien if you’re underwater, including how to bridge the cash gap to settle your debt.

- Discover how to get a nationwide cash offer where the buyer handles all DMV and bank paperwork for you.

Understanding the Logistics of Selling an RV with a Lien

You might have the keys in your pocket and the vehicle in your driveway, but if you have an active loan, you don’t fully own the asset yet. The bank or credit union is the legal owner until that balance hits zero. This legal claim is known as a lien. If you’re curious about the technical definition, you can read more about What is a Lien? and how it functions as a security interest. Selling a motorhome I still owe money on is entirely possible, but it requires a different set of steps than selling a vehicle with a clear title in hand.

A clear title sale is a simple exchange of cash for paperwork. A financed title sale is a three-way coordination between you, the buyer, and the lender. Private buyers are often hesitant to step into this triangle. They want to drive away with the title, not a promise that it will arrive in the mail weeks later. Most banks won’t release the title until the funds have cleared and the account is closed. This creates a “Trust Gap” that kills most private deals before they even start. To bridge this gap, you need a Payoff Letter. This official document from your bank proves they’re ready to release the lien once they receive a specific amount of cash.

What is a 10-Day Payoff Quote?

RV loans are dynamic. Interest accrues every single day, which means your balance on Monday won’t be your balance on Friday. You can’t rely on your monthly statement to calculate your equity. You must request a formal 10-day payoff quote from your lender. This document freezes the amount for a ten-day window, giving you a fixed target for the sale. It dictates your “walk-away” cash amount. If a buyer offers you $75,000 and your payoff is $68,000, you know exactly how much stays in your pocket after the bank gets their share.

The Legal Risks of Private Lien Transfers

Selling a motorhome I still owe money on to a stranger involves significant risk. Buyers hate paying for a vehicle they can’t legally own on day one. They fear you’ll take their money and disappear without paying off the loan. On the flip side, you face the risk of unverified third parties or fraudulent checks that don’t actually clear the bank. Dealing with these logistics is a full-time job. The lien release period is typically 10 to 30 business days. Most private buyers aren’t willing to wait a month for their paperwork while their cash is already spent. This is why professional acquisition is the standard for owners who want a secure, immediate exit from their loan.

The Step-by-Step Process of Handling a Bank Payoff

Forum advice often tells you to just meet the buyer at a local bank branch. That’s outdated. Many major lenders like Ally or Bank of America don’t even have physical branches in your town. You need a modern, streamlined process for selling a motorhome I still owe money on that works regardless of where your lender is located. This process ensures the bank gets paid, the buyer gets the title, and you get your cash without legal loose ends.

- Step 1: Request your official 10-day payoff amount. Call your lender’s total loss or payoff department to get a written statement of the exact balance including daily interest.

- Step 2: Determine your equity position. Compare your payoff amount to your highest cash offer. Positive equity means you walk away with a check; negative equity means you’ll need to pay the difference.

- Step 3: Secure a buyer who understands the lien process. Professional buyers deal with liens daily, while private buyers often get cold feet when they realize they won’t have the title immediately.

- Step 4: Execute the Bill of Sale and Power of Attorney. These documents allow the buyer to handle title processing with the DMV once the bank releases the lien.

- Step 5: Facilitate the direct bank-to-bank wire transfer. This is the fastest way to stop interest from accruing and trigger the title release.

If this sounds like a mountain of paperwork, you can skip the stress and get a professional cash offer that handles every detail for you. Adhering to state regulations for selling a vehicle with a lien ensures you stay legally protected during the transfer.

Coordinating with Your Lender

National lenders operate differently than local credit unions. While a local branch might sign off on a title in person, national banks require a Letter of Authorization. This document gives your buyer permission to discuss the payoff details with the bank. Don’t cancel your insurance the moment you sign the Bill of Sale. Keep coverage active until the bank confirms the loan is closed and the wire has cleared. This protects you during the 10 to 30 business days it typically takes for the title to move through the system.

Executing the Paperwork Correcty

A secure Bill of Sale is your primary defense. It must clearly state that the vehicle is being sold “subject to lien payoff.” You’ll also need a Limited Power of Attorney for motor vehicle transactions. This specific form allows the buyer or their agent to sign the title on your behalf once the bank mails it out. Double-check the mailing address the bank has on file. You want the lien release and title sent directly to the new owner or the processing agency to avoid unnecessary delays in the 2026 market.

Private Sale vs. Professional Acquisition: Which Handles Debt Better?

Private sales promise the highest price on paper, but they rarely deliver when a bank owns the title. Vetting a buyer who can actually secure a $100,000 loan for a Class A motorhome is a logistical nightmare. Most private buyers don’t have that kind of cash sitting in a checking account. They need their own financing, which means two different banks must now coordinate a title transfer. This doubles the paperwork and triples the time it takes to close the deal. You’re left managing the “Trust Gap” while the buyer waits for a title that you don’t even have in your possession.

When you’re selling a motorhome I still owe money on, speed is your best friend. Every month the unit sits on the market, you’re paying high interest rates, which can reach nearly 36% for some borrowers in 2026. A professional acquisition company closes the loan immediately. We specialize in complex Class A and Class C payoffs that scare away individual buyers. While a private sale might take 60 to 90 days to finalize, a professional cash offer can be completed in a fraction of that time. You can find a complete guide to selling your RV that outlines these hurdles, but few mention the specific burden of carrying a loan during the listing period.

The Problem with RV Consignment and Loans

Consignment might seem like a hands-off solution, but it’s often a trap for owners with active loans. Most shops won’t prioritize your unit if the payoff is high because their commission is squeezed. You’ll continue making monthly payments and paying for insurance while the RV sits on a lot. It’s better to understand the logic of RV Consignment vs. a Direct Cash Sale before you commit. A direct sale stops the bleeding of interest and depreciation instantly. We take the vehicle off your hands and settle the debt so you can stop paying for an asset you no longer use.

Why Dealers Offer Less for Financed Units

Traditional dealerships often use your loan balance against you. They see your debt as a point of leverage to lower their offer, knowing you’re eager to exit the loan. They might also tack on “prep fees” or “documentation fees” that can reach $999 in states like Florida. A clean, direct cash purchase from a professional buyer eliminates these hidden costs. We provide a transparent offer that respects your equity without the “Trade-In Trap” games. We focus on the fair market value of your Class B or Class C motorhome, not how much you happen to owe the bank.

What to Do If You Are Underwater on Your Motorhome Loan

Being “underwater” on a loan is a common reality in the 2026 RV market. This means you owe the bank more than the vehicle is currently worth. It often happens because motorhomes depreciate faster than loan balances decrease, especially with the high interest rates seen in early 2026. Many online forums will tell you that you’re stuck, but that isn’t true. Selling a motorhome I still owe money on while in a negative equity position just requires a clear strategy to bridge the gap.

You have two primary options when facing negative equity. The first is paying the “Cash Gap” to clear the title. This involves paying the difference between the sale price and your loan balance out of pocket. It’s often the smartest financial move because it stops the bleeding of monthly interest and insurance costs immediately. The second option is rolling the balance into a new loan. We generally advise against this. It traps you in a cycle of debt where you’re paying for a vehicle you no longer own. A professional appraisal is your best tool here. It provides a concrete number that helps you minimize the gap and avoid leaving money on the table.

Calculating Your Net Exit Cost

Don’t guess your financial standing. Use this simple formula to find your exact position: [Current Loan Balance] – [Cash Offer] = Your Exit Cost. If your loan is $80,000 and the cash offer is $72,000, your exit cost is $8,000. Securing a high cash offer is critical to keeping this number as low as possible. To get a better sense of what your unit is worth before you talk to a lender, check out our guide on How to Value Your RV. Knowing the market value prevents you from accepting a lowball offer that unnecessarily inflates your out-of-pocket costs.

Strategies for High-Value Class A Motorhomes

Class A units are the heavyweights of the industry, but they also see the steepest depreciation. With average wholesale values for motorhomes sitting in the low-$60,000 range in early 2026, many luxury owners find themselves with significant loan balances. Market trends show a shift toward affordability, which puts extra pressure on the resale value of high-end diesel pushers. Professional buyers often pay more for well-maintained Class A units than local dealers because they have a nationwide network to move the inventory. If you want to stop the depreciation and settle your debt today, request your instant cash offer now and let us handle the bank logistics for you.

How RV Buyers USA Simplifies Selling a Motorhome with a Loan

Selling a motorhome I still owe money on doesn’t have to be a multi-month ordeal. While private sales and dealerships create friction, RV Buyers USA removes the middleman and the stress. We act as your professional problem solver, handling all bank communications and payoff logistics from start to finish. You don’t need to spend hours on hold with your lender or try to navigate complex DMV regulations alone. Our team understands the 2026 market and the urgency of closing out high-interest loans that can reach nearly 36% for some owners. We bridge the trust gap by providing a secure, corporate-backed transaction that protects your financial interests.

- Direct lender coordination to secure and verify the 10-day payoff amount.

- Nationwide service that brings the closing table directly to your driveway.

- Immediate cash offers that prioritize settling your debt and maximizing your equity.

- Professional management of all title transfers, lien releases, and DMV paperwork.

The “We Come to You” Advantage

Forget the logistics of driving your Class A, B, or C motorhome to a dealership or a bank branch. We provide a truly nationwide service that spans every state. Our experts travel to your location for a free appraisal and professional inspection. This removes the risk of driving a high-value asset across state lines just to get a quote. We verify the condition, finalize the offer, and ensure you receive secure payment before we ever hitch up and head out. It’s a transparent, face-to-face transaction that prioritizes your safety. You get the peace of mind that comes with a professional “we come to you” service, saving you time and travel expenses.

Start Your No-Hassle Sale Today

Ready to exit your loan? Getting started takes only a few minutes. We just need basic information about your motorhome, such as the make, model, and current mileage, along with your lender’s name. We’ll handle the heavy lifting of calculating the payoff and drafting the Bill of Sale. You can stop worrying about high monthly payments and the depreciation pressure affecting used inventory in 2026. Our process is the fastest and most reliable way of selling a motorhome I still owe money on. We move from initial contact to a completed sale in days, not months. Take the first step toward a clean break from your bank today. Get a Cash Offer for Your Motorhome Now and let our seasoned experts clear your title for you.

Secure Your Professional Exit and Clear Your Debt Today

You now have the roadmap to navigate the complex world of bank liens and negative equity. Don’t let the weight of high interest rates or the fear of being underwater keep you from moving forward. Selling a motorhome I still owe money on is a streamlined process when you partner with experts who understand the 2026 market. We’ve been professional problem solvers since 2003; our team brings over two decades of acquisition expertise to every single transaction. We specialize in managing high-value Class A, B, and C motorhome payoffs with zero paperwork stress for the owner. Our free nationwide pickup and professional paperwork management ensure you stay home while we do the heavy lifting. We handle the DMV, coordinate directly with your lender, and ensure the wire clears before we leave your driveway. It’s time to stop making payments on an asset you no longer need. Take the first step toward a hassle-free closing and a fair price for your vehicle. Get an Instant Cash Offer and Let Us Handle Your RV Loan Payoff. You’re just one click away from a clean title and the financial freedom you deserve.

Frequently Asked Questions

Can I sell my RV if the loan is more than the value?

Yes, you can sell an underwater RV by paying the difference between the sale price and the loan balance. This “cash gap” must be settled with the lender before they release the lien. If you’re selling a motorhome I still owe money on, a professional buyer can help coordinate this payment to ensure the account is closed correctly. It stops the cycle of high interest and depreciation immediately.

How long does it take to get the title back from the bank after selling?

You can expect to receive the title from the bank within 10 to 30 business days after the final payoff is processed. The exact timing depends on whether the lender uses electronic titles or physical paper documents. If you’re dealing with a national bank, they often mail the title directly to the new owner or the state DMV. Always verify the mailing address with your lender during the payoff request.

Does the buyer pay the bank or me directly?

The buyer should pay the lender directly for the outstanding balance to ensure the lien is cleared. Any remaining funds from the agreed sale price are then paid to you as profit. This structure protects the buyer’s interest and guarantees the bank receives its money. When we handle your acquisition, we manage this bank-to-bank wire transfer to provide a secure and transparent closing for both parties.

What paperwork do I need to sell a motorhome with an outstanding loan?

You’ll need a formal 10-day payoff quote, a secure Bill of Sale, and a Limited Power of Attorney for motor vehicle transactions. Most lenders also require a signed Letter of Authorization to discuss account details with the buyer. These documents allow the new owner to process the title once the bank releases the lien. Having these ready prevents delays and keeps the transaction moving quickly in the 2026 market.

Can I sell my financed RV to a private party out of state?

Yes, you can sell to an out-of-state private party, but it significantly increases the paperwork burden. Each state has unique title and lien laws, such as Texas title fees or Florida’s $77.75 new title fee. Coordinating a lien release across state lines often leads to weeks of delays. Professional nationwide buyers simplify this by managing all state-specific DMV requirements and picking up the vehicle directly from your door.

What happens if I sell my RV but don’t pay off the loan?

Selling the vehicle without paying off the loan is a violation of your contract and often constitutes legal fraud. The bank remains the legal owner, and the lien stays attached to the title. The new buyer won’t be able to register the vehicle or obtain a clean title in their name. This usually leads to legal action from the buyer and a total loss of your credit standing.

Will selling my motorhome for less than the loan hurt my credit?

Selling for less than the loan balance won’t hurt your credit as long as you pay the difference to the bank. Your credit score is only impacted if you stop making payments or negotiate a short sale where the bank agrees to accept less than the full balance. If you clear the account in full during the sale, it shows as a successfully closed loan on your credit report.

Do I need to notify my lender before I list my RV for sale?

No, you don’t need to notify your lender just to list the vehicle for sale. However, you should contact them as soon as you have a serious buyer to request a written 10-day payoff quote. This document is essential for selling a motorhome I still owe money on because it provides the exact figure needed to close the account. Early communication helps you understand the bank’s specific requirements for title release.