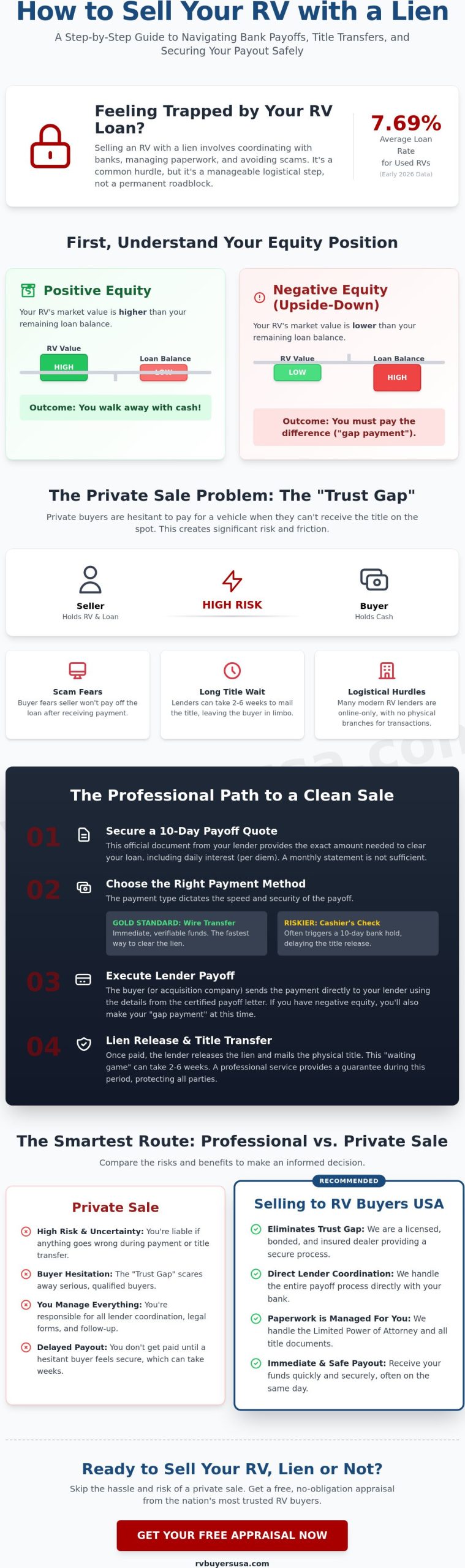

Your bank holding the title shouldn’t feel like a prison sentence for your driveway. You want to move your asset quickly, but the thought of coordinating bank wires, avoiding scams, and managing DMV paperwork feels like an exhausting hurdle. It’s especially daunting when you’re facing high interest rates; the average RV loan rate for used units hit 7.69% in early 2026. You likely feel stuck between a high payoff balance and a market where values are normalizing. Learning how to sell an rv with a lien is simply a matter of following a professional process rather than leaving it to chance.

This guide provides the exact steps to navigate bank liens, coordinate directly with lenders, and secure a safe payout even if you’re upside-down on your loan. We’ll break down how to clear your debt, manage the title transfer legally, and avoid the administrative headaches that typically derail private sales. Whether you’re moving a Class A motorhome or a travel trailer, you’ll learn how to bridge the trust gap with a professional acquisition strategy that ensures immediate liquidity and a clean break from your lender.

Key Takeaways

- Recognize that a bank lien is a manageable logistical step, not a legal barrier to selling your motorhome or trailer.

- Master the timing of your transaction by securing a 10-day payoff quote from your lender to lock in your exact debt obligation.

- Learn how to sell an rv with a lien safely by using professional acquisition channels that bypass the risks and delays of the private market.

- Navigate the differences between wire transfers and cashier’s checks to ensure your loan is cleared without unnecessary holding periods.

- Simplify the paperwork process by leveraging a service that manages the Limited Power of Attorney and direct lender coordination for you.

Understanding the RV Lien Sale Process

Selling a vehicle you don’t technically own yet can feel like a legal maze. However, thousands of motorhomes and trailers change hands every month while still under finance. To understand what is a lien? in this context, think of it as a security interest. Your lender holds the title as collateral until the debt is satisfied. While it adds a layer of administration, knowing how to sell an rv with a lien is a standard professional procedure in all 50 states. The objective is simple: secure the funds, pay the lender, trigger the lien release, and move the title to the new owner. You aren’t just selling a vehicle; you’re orchestrating a debt settlement and a title transfer simultaneously.

The Difference Between Positive and Negative Equity

Your financial standing determines your strategy. Positive equity occurs when your RV’s market value is higher than your loan balance. This is the ideal scenario. You walk away with cash in your pocket. Negative equity, often called being “upside down,” is more complex. This happens when you owe the bank more than the current market value. In early 2026, many owners found themselves in this position as wholesale values normalized and interest rates climbed. If you’re underwater, you must provide a “gap payment” to the bank. The lender won’t release the title until the full balance is paid, even if the sale price doesn’t cover it. You need to have those funds ready before you initiate the sale to avoid a collapsed deal at the finish line.

Why Private Buyers Are Often Hesitant

Private sales with liens are difficult because of the “Trust Gap.” Most individual buyers are terrified of handing over thousands of dollars without receiving a title on the spot. They fear a scenario where the seller pockets the cash and stops making payments, leaving the buyer with a vehicle they can’t legally register. This risk is real. For a private transaction to work safely, it usually requires a bank-to-bank transfer or a meeting at the lender’s local branch. This logistical burden often causes private buyers to walk away in favor of a cleaner deal. Most people don’t want the liability of waiting weeks for a bank to mail a title. Professional acquisition services eliminate this friction by handling the debt payoff directly with your financial institution, providing a level of security that a private buyer simply can’t match.

The Logistics of Paying Off a Loan During a Sale

The mechanics of debt satisfaction require precision. You cannot simply hand over a title you don’t possess. Instead, you must coordinate with your lender to ensure every cent of interest is accounted for. This starts with a 10-day payoff quote. This document calculates the principal balance plus the daily interest, known as per diem, accrued over the next ten days. It provides a fixed target for the buyer’s payment and ensures the account is settled to the penny.

Payment methods dictate your speed. A bank wire transfer is the gold standard because it provides immediate, verifiable funds. Cashier’s checks are common but often trigger a 10-day clearance rule. Lenders frequently hold the title until the check fully clears their internal systems. If you are dealing with a high-value Class A motorhome or a luxury fifth wheel, consider using a third-party escrow service. This provides a neutral vault for the funds until the lender confirms the payoff is complete. While many online forums suggest meeting at a local bank branch to finalize the deal, this advice often fails. Many modern RV lenders are online-only institutions with no physical storefronts. In these cases, digital coordination is your only path.

If you want to skip the administrative burden of tracking down lenders and managing wire transfers, you can sell your RV directly to a professional firm that handles these digital hurdles for you.

Securing a Certified Payoff Letter

A standard monthly statement is insufficient for a legal transaction. It doesn’t reflect the daily interest that accumulates between the statement date and your actual sale date. A payoff letter is the official bank-issued balance required to satisfy the loan in full. Ensure your letter includes the lender’s wiring instructions, the daily interest rate, and a clear expiration date. Without this certified document, the bank may reject a payment that is even a few dollars short, stalling the entire transfer.

The “Waiting Game” for Title Release

Paying the bank doesn’t result in an instant title. Most lenders take 2 to 6 weeks to process the paperwork and mail the physical title to the new owner. This delay is the primary source of anxiety for buyers. To mitigate this, provide the buyer with a Lien Release document or a formal letter of guarantee from the bank. Managing these expectations is critical when figuring out how to sell an rv with a lien without losing your buyer. Clear communication about DMV processing times prevents the sale from souring after the money has changed hands.

Private Sale vs. Professional Acquisition: The Trust Gap

Selling to an individual requires you to act as a part-time loan officer and a full-time debt negotiator. Most private buyers are looking for a simple exchange: cash for a title. The moment they hear you have a lien, the trust gap widens. They worry about your ability to clear the debt and fear a scenario where they pay you but never receive the legal ownership documents. This hesitation is why many private listings for motorized and towable units sit for months. In a market that saw a 24.12% year-over-year decline in early 2026, you cannot afford to let a qualified buyer walk away because of paperwork anxiety.

The liability risks in a private sale are significant. If the bank experiences a delay in releasing the title, the buyer may hold you legally responsible. You are the one stuck making the phone calls, tracking the mail, and managing the buyer’s growing frustration. Professional acquisition firms close this gap by assuming the administrative burden. While a private sale can take weeks of back-and-forth, a professional buyer can often close the deal in 24 hours. They move with the speed of a business rather than the uncertainty of an individual, providing immediate liquidity and a clean break from your loan obligations.

Common Scams to Avoid in Lien Sales

Scammers exploit the complexity of bank-held titles. One prevalent tactic is the overpayment scam. A “buyer” sends a cashier’s check for more than the agreed price, asking you to wire the excess to a “shipper” or to pay off the lien immediately. These checks are almost always fraudulent. By the time your bank realizes the check is fake, you’ve already wired real money from your own account. Other buyers may pressure you to let them take possession of the motorhome before the lien is cleared. Never release the vehicle until the bank confirms the loan is satisfied and you have the remaining equity in hand. Always verify a buyer’s funds through a direct bank-to-bank call before sharing your lender’s payoff information.

The Professional Advantage

Working with a bonded and insured firm eliminates the guesswork of how to sell an rv with a lien safely. These organizations deal with major lenders daily and understand the specific requirements for Class A, B, and C motorhomes. They use “One-and-Done” transactions where they pay your lender directly and hand you a check for your equity on the spot. This removes you from the middle of the transaction and ensures the bank is satisfied immediately. Before you list your unit, use these selling my rv valuation tips to understand your current market standing. A professional buyer provides a guaranteed exit strategy without the liability, scams, or administrative headaches of the open market.

Step-by-Step: How to Coordinate with Your Lender

Executing a sale while a bank holds the title requires a disciplined sequence of actions. You aren’t just handing over keys; you’re managing a financial closing. Follow these five steps to ensure the transaction remains secure and legally sound.

- Step 1: Call your lender’s payoff department to request an official 10-day payoff quote. This document must include the daily interest rate and specific wiring instructions.

- Step 2: Sign a Limited Power of Attorney. This document is the linchpin of the sale, as it authorizes the buyer to process the title paperwork with the DMV once the bank releases it.

- Step 3: Draft and sign a Bill of Sale. This contract must explicitly state the purchase price, the amount being sent to the lender, and any remaining equity being paid to you.

- Step 4: Facilitate the payment. The buyer should send funds directly to your lender via a bank wire to ensure immediate debt satisfaction.

- Step 5: Obtain a copy of the wire confirmation. Do not release the vehicle until you have this digital receipt and have verified the payoff with your bank’s representative.

If you prefer to bypass this coordination entirely, you can sell your motorhome or trailer to a professional buyer who manages the bank communication and paperwork for you.

Essential Paperwork for a Lien Sale

A successful sale relies on a complete document package. Your Bill of Sale must include the Year, Make, Model, VIN, and current mileage. You also need a Limited Power of Attorney form. This is essential because the physical title won’t be available on the day of the sale. By signing this, you give the buyer the legal right to act on your behalf at the DMV once the bank finally mails the document. Finally, don’t forget the Odometer Disclosure Statement. This is a federal requirement for most RVs and protects both parties by creating a legal record of the vehicle’s usage at the time of transfer.

Communicating with Your Bank’s Lien Department

The bank is the legal owner until the lien is released. Because of this, you must be proactive in your communication. Immediately after the wire is sent, call the bank to confirm receipt and request a “Lien Satisfaction” letter. This document serves as your proof that the debt is gone while you wait for the state to process the new title. Ensure the bank has the correct mailing address for the new owner or the professional acquisition firm. Double-checking this detail prevents the title from being sent to your home by mistake, which would cause significant delays in the legal transfer of ownership.

Why Selling to RV Buyers USA is the Easiest Way to Clear a Lien

Managing a bank-held title on your own is a full-time job. You’ve seen the risks of the private market and the complex paperwork required by lenders. We provide a streamlined alternative that removes the friction from the transaction. We specialize in the acquisition of Class A, Class B, and Class C motorhomes with existing bank loans. Our team also handles Fifth Wheels, Travel Trailers, and Toy Haulers. Instead of you spending hours on hold with a lien department, we take over the communication. We coordinate the payoff, verify the wire instructions, and ensure the bank releases the title correctly. This professional approach turns a weeks-long ordeal into a rapid, secure transaction.

Logistics shouldn’t be your problem. Many sellers worry about how to move a high-value asset while the bank still holds the legal claim. We offer free nationwide pickup. It doesn’t matter if your RV is in a storage lot in Florida or your driveway in Washington; we come to you. This service eliminates the need for you to drive to a dealership or meet strangers in parking lots. We handle the physical acquisition and the administrative burden simultaneously. You avoid the stress of DMV lines and the anxiety of title transfer errors. We act as the problem solver, providing a clean break from your loan and immediate liquidity for your asset.

Immediate Cash Offers and Bank Coordination

Our process is built for speed. We calculate your equity by comparing our professional appraisal against your 10-day payoff quote. If you have positive equity, we pay you the difference instantly. Our “Fast-Track” payoff process is designed to bypass the traditional 10-day waiting periods often found in retail environments. We use secure, verifiable bank wires to satisfy your debt immediately. This ensures your credit is protected and your loan is closed without delay. You get the security of dealing with an established acquisition firm that understands how to sell an rv with a lien better than any private buyer ever could.

Get Your Free Appraisal Today

Stop waiting for the perfect private buyer who isn’t afraid of a lien. The used RV market is shifting, and waiting only risks further value normalization. Our process is simple. Submit your vehicle details, receive a fair market offer, and let us handle the bank. You won’t deal with the hassles of retail sales, the long wait times of consignment, or the liability of a private transaction. We provide a guaranteed exit strategy that puts cash in your pocket and clears your debt. Get a fast cash offer and clear your RV lien today and experience the most efficient acquisition service in the industry.

Secure Your Exit Strategy and Clear Your Debt Today

Selling a high-value asset with a bank-held title doesn’t have to be a logistical nightmare. You now understand that a lien is simply a hurdle that requires the right coordination, specifically 10-day payoff quotes and Limited Power of Attorney forms. While private sales are often stalled by the trust gap, you have a faster and more secure path to liquidity. Knowing how to sell an rv with a lien allows you to stop worrying about market shifts and start focusing on your next chapter. The process is simple.

Our A+ rated professional acquisition team specializes in clearing these debts quickly. We include nationwide pickup at no cost to you. Our experts handle all DMV and title paperwork, ensuring a legal and seamless transfer. We handle the bank so you don’t have to. This is the most efficient way to move your Class A, B, or C motorhome or trailer without the administrative headache. Get a Professional Cash Offer for Your RV and Clear Your Lien Fast. Take the first step toward a clean title and immediate cash today.

Frequently Asked Questions

Can I sell my RV if I owe more than it is worth?

Yes, you can sell an “upside-down” RV by paying the difference between the sale price and the loan balance directly to the lender. This is common when wholesale values normalize, as seen in early 2026. The bank won’t release the title until they receive the full payoff amount. Ensure you have these funds available before finalizing the transaction to avoid a collapsed deal.

How long does it take for a bank to release an RV title after payoff?

Expect to wait 2 to 6 weeks for the physical title to arrive after the loan is satisfied. Most lenders process the lien release electronically through the DMV first. If you need to prove the sale in the interim, use a bank-issued Lien Satisfaction letter. This document confirms the debt is gone while the state catches up with the paperwork.

Does the buyer pay the bank or the seller in a lien sale?

The buyer should pay the bank directly via a wire transfer to ensure the lien is cleared. This is the safest way to navigate how to sell an rv with a lien because it eliminates the risk of the seller pocketing the cash. Any remaining equity after the bank is paid is then issued to the seller. This tiered payment structure protects both parties and satisfies the legal owner first.

Is a Bill of Sale enough to prove ownership if the bank has the title?

A Bill of Sale records the transaction, but it doesn’t replace the title as legal proof of ownership. The title remains the ultimate authority in the eyes of the DMV. You need the Bill of Sale to document the transfer of possession and price, but the new owner cannot register the vehicle until the bank releases the actual title. Always provide a Limited Power of Attorney to help the buyer bridge this gap.

What happens to my insurance once the lien is paid off?

Cancel your insurance only after the bank confirms the payoff and the vehicle has been picked up by the new owner. Don’t stop coverage the moment the wire is sent. You are responsible for the asset until the lender issues the lien release and the buyer takes possession. Once the transfer is complete, notify your agent to avoid paying premiums on a vehicle you no longer own.

Do I need to notify the DMV that I sold an RV with a lien?

Yes, you must file a Notice of Transfer and Release of Liability with your state’s DMV immediately. This protects you from future tickets, registration fees, or liability issues involving the vehicle. Even if the bank hasn’t mailed the new title yet, this filing puts the state on notice that you are no longer the operator. It’s a critical step in finalizing how to sell an rv with a lien correctly.

Can I sell an RV with a lien to a dealer?

Yes, selling to a professional acquisition firm or dealer is often the fastest way to clear a debt. Professional buyers handle the bank coordination, wire transfers, and DMV paperwork as part of their service. This removes the administrative burden from your shoulders. It’s an efficient alternative to private sales, where individual buyers often lack the funds or patience to deal with a bank-held title.

What is a 10-day payoff quote and why do I need it?

A 10-day payoff quote is an official statement from your lender that includes the principal balance and the daily interest accrued over the next ten days. You need this because standard monthly statements don’t account for the daily interest that builds up. It provides a fixed, accurate number for the buyer’s wire transfer. Without it, your payment might be short, which prevents the bank from releasing the title.